2 all recorded transactions are valid. AIS Exam 2 - Expenditure Cycle.

Accounting Information Systems 9 Th Edition Marshall B

HAPTER 11 The Expenditure Cycle.

Expenditure cycle ais. Chapt er 3 The Expenditure Cycle Part I. Recurring set of business activities and related data processing operations associated with the purchase of and payment for goods and services. 5 assets are safeguarded from loss or theft.

View AIS Chapter 3 The Expenditure Cyclepdf from ACCOUNTANC 123 at Polytechnic University of the Philippines. Minimize the total cost of acquiring and maintaining inventories supplies and the various services the organization needs to function Expenditure Cycle Activities 1. Determine when and how much additional inventory to order.

The AIS should provide decision making information to. In an Accounting information systems TPS is the most fundamental system that is responsible for recording of Transaction in Journals and vouchers and distributing necessary information for daily operations. Expenditure Cycle MONITOR INVENTORY RECORDS Firms deplete their inventories by transferring raw materials into the production process conversion cycle and by selling finished goods to customers revenue cycle prepared and sent.

B a customer sale. IS An Accountant Perspective. Purchasing efficiency and effectiveness Supplier performance Time taken to move goods from receiving to production Percent of.

Purchases and Cash Disbursements Procedures 217 THE CONCEPTUAL SYSTEM 218 Overview of Purchases and Cash Disbursements Activities 218 The Cash Disbursements Systems 225 Expenditure Cycle Controls 228 PHYSICAL SYSTEMS 230 A Manual System 230 The Cash Disbursements Systems 232 COMPUTER-BASED PURCHASES. Learning Objective 1 Difficulty. The Transaction Cycle model is one way to view basic business processes.

D receiving goods from vendors. Expenditure Cycle a recurring set of business activities and related data processing operations associated with the purchase of and payment for goods and services Primary objective in the. Expenditure cycle Interactions with suppliers.

- it is the set of business activities which involve purchasing decisions and actions - their data processing operations involved are correlated with the purchases and payments of goods and services. Revenue expenditure production human resourcespayroll and financing. 3 all valid and authorized transactions are recorded.

Human resourcespayroll cycle Give cash. AIS Separation of Duties. C shipping goods to customers.

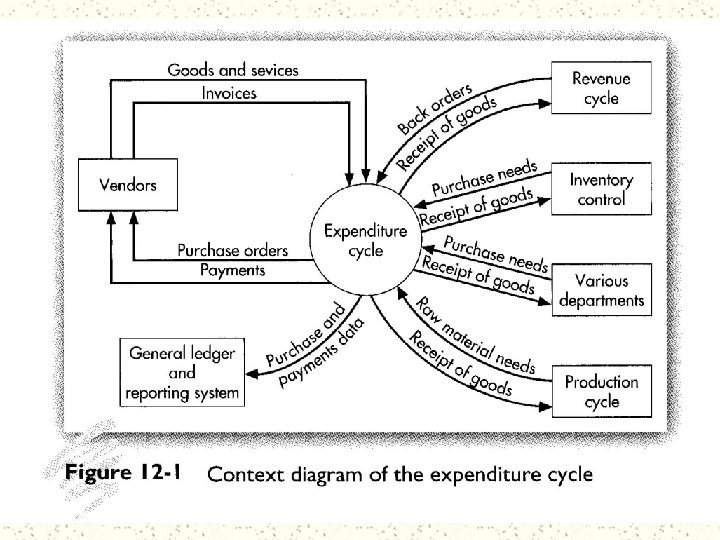

The expenditure cycle is the set of activities related to the acquisition of and payment for goods and services. Purchasing Cash Disbursements. The objective of the expenditure cycle is to convert the organizations cash into physical materials and human resources it needs to conduct business.

There are three main Subsystems of TPS including the revenue cycle the expenditure Cycle and the conversion cycle. Select the appropriate vendors from whom to order. Expenditure cycle information system Objective.

Much of the input to the expenditure cycle comes from the sales cycle where purchasing requirements are. AIS Overview of AIS. Purchasing and Cash Disbursements.

On-line data entry with edit controls. On-line processing with an integrated database for JIT or MRP system. Figure 2-1 shows the flow of cash from the organization to the various providers of these resources.

Purchasing and Cash Disbursements 2. 1 all transactions are properly authorized. IT opportunities for use of.

These activities include the determination of what needs to be purchased purchasing activities the receipt of goods and payments to suppliers. What types of decision-making and strategic information should the AIS provide in the expenditure cycle. Financing cycle Give cash.

AIS P4-1 Revenue Cycle. The expenditure cycle part ii As mentioned in the prior chapter the expenditure cycle is concerned with the acquisition of fixed assets raw materials or manufactured components and the use of employee labor to. Types of transaction processing system in AIS.

In this chapter we concentrate on systems and procedures for acquiring raw materials and finished goods from suppliers. 2006 Prentice Hall Business Publishing Accounting Information Systems 10e RomneySteinbart 117 of 122 EXPENDITURE CYCLE INFORMATION NEEDS The AIS needs to provide information to evaluate the following. AIS The Revenue Cycle.

Ais Romney 2006 Slides 11 The Expenditure Cycle 1. ETHICS THE BEST SOLUTION. In the expenditure cycle Accounting Information System AIS should provide internal and external controls to ensure that the following objectives are met.

For instance every business 1 incurs expenditures in exchange for resources cash purchases expenditure cycle 2 pays out money for services rendered by employees and acquisition of fixed assets the payroll and fixed assets cycle 3 provides value added through its products or services conversion cycle 4 receives revenue from outside sources revenue cycle. What is the expenditure cycle. Accounting Information Systems presentation detailing the Expenditure Cycle for RCJC Chic Shoe Boutique located in New York City.

What will be an ideal response. Business activities begin with the acquisition of materials property and labor in exchange for cashthe expenditure cycle. Purchasing and payment of Goods and services.

Production cycle Give labor and raw materials. Chapter 5 The Expenditure Cycle Part I. 4 all transactions are recorded accurately.

In the expenditure cycle or any cycle a well-designed AIS should provide adequate controls to ensure that the following objectives are met. The Expenditure Cycle. Transaction processing system definition.

Most expenditure transactions are based on a credit relationship between the trading par- ties. 9 The first major business activity in the expenditure cycle is A ordering inventory supplies or services. HAPTER 11 The Expenditure Cycle.

All transactions are properly authorized All recorded transactions are valid. Purchases and Cash DisbursementsProcedures the. The purpose of The AIS Transaction Cycles Game is to provide drill and practice or review of the elements that comprise the five typical transaction cycles identified as.

The Expenditure Cycle The Expenditure Cycle Activities and information processing related to.

Accounting Information Systems 9 Th Edition Marshall B

Acct 316 Acct 316 12 Chapter Acct 316